Why I Built FutureClear

My first job was as a musician. I loved it, but making enough money to cover rent, bills, and a social life was a constant struggle. Which is how I ended up in financial services in my twenties.

I joined a startup as a business analyst, working on complex financial products. This was the 1990s. I spent a few years learning the industry from the inside: how products are actually designed, what customers care about, and what the systems underneath look like when nobody outside the company is watching. It was a better education than any course I could have taken.

The frustrating part was handing my designs over to an IT team and waiting to see what came back. Software development in the 1990s wasn’t the discipline it is today; the gap between what I specified and what I got was usually wide enough that it was easier to start writing code myself than to keep re-specifying every detail. Evenings and weekends for a few years, learning enough to be useful, then taking on more of the implementation work.

Over the next twenty-five years I built a career in financial services technology, eventually running engineering teams at a Fortune 100 financial services company, on systems used every day by millions of people. I won’t go into specifics in this blog post, but the relevant thing about that world is the discipline you pick up. It’s no fun when your pager goes off at 3 a.m. because your buggy IT systems broke down. It soon gives you a healthy fear of getting the code wrong.

When I went looking

A couple of years ago I started thinking seriously about early retirement. My wife and I needed to understand what our financial timeline actually looked like — what we had, when we could access which pots, how UK tax would bite in different years. I assumed there would be a tool for this.

Between us we have a handful of pensions, some ISAs, a house, different levels of income, and different ideas about when each of us wants to stop work. I wanted to see what we’d actually have available to spend in each year between now and our eventual demise, after income tax, capital gains tax, dividend tax and any taper effects from the Personal Allowance. I wanted to be able to change an assumption and watch what it did to the outcome.

The tools I tried fell into two groups. The first was free calculators aimed at the general population: enter a few numbers, get a single headline figure back. There’s no real tax modelling in these, no way to represent multiple pots with different access ages, no way to capture life events like downsizing or a partner retiring earlier than you do. They’re designed to produce a plausible-looking answer from minimal input, not to help anyone plan.

The second group was more serious: paid retirement planning tools, most of them built for the US market. Some of these are genuinely good if you’re American. For a UK household they break down almost immediately. They don’t know what a SIPP is. They model 401(k)s and IRAs with tax rules that don’t apply here. UK-specific mechanics like the Personal Allowance taper, ISA allowances, and crystallisation of Defined Contribution pensions aren’t represented at all.

A financial adviser would have solved some of the problem. I’ve worked with advisers before and I know where the value is — they’re useful for the big decisions and for catching tax traps you might have missed. But I always felt that I paid over the odds for an occasional review meeting where, more often than not, they just confirmed what I already knew. What I actually wanted was a place to try different assumptions myself and watch the knock-on effects play out over thirty-five years. That’s a tool job, not an adviser job, and no tool existed. Eventually I stopped looking and started building.

A tool for two people

The first version of FutureClear was a private tool for the two of us. I wrote it to model our specific situation — both partners, our actual pensions and ISAs, the spending patterns we expected, and the life events that would shift things year by year (my wife is a little older than me, so she accesses her pension first; a downsizing move we’d been discussing; the year I planned to stop full-time work).

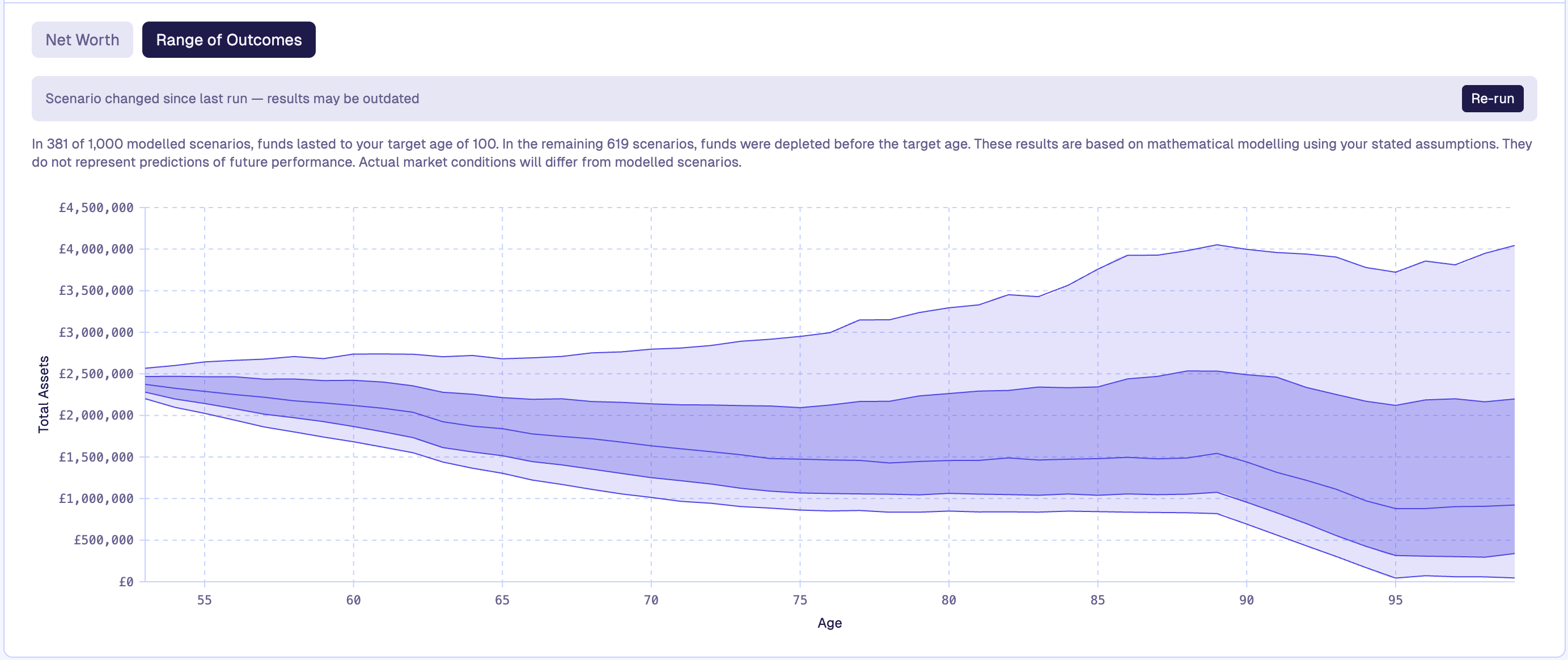

The engineering side I took seriously because it’s the part I know how to do. Tax is calculated per partner and per year against actual HMRC rules. The Monte Carlo engine runs a thousand randomised simulations with returns drawn from a historical distribution, so the output is a range of outcomes rather than a single optimistic line. The year-by-year table shows the full mechanics — income, tax, contributions, withdrawals, capital gains accrual and realisation — not just the net figure at the end.

It worked. For the first time I could see our financial timeline thoughout our full lifetimes laid out in a single table, with every assumption changeable.

Then I looked around

Once I had something that worked for us, I started paying attention to the wider picture. I’d been reading the UK personal finance subreddits for a while — r/UKPersonalFinance and r/FIREUK mostly — and I started noticing how often the same questions came up. “How much do I need to retire?” “Should I draw from my SIPP or ISA first?” “How will tax work if my wife retires before me?” “Can I afford to stop at 57?” The same questions appeared on Money Saving Expert, in the FIREUK forums, and underneath every UK retirement YouTube video I watched.

What struck me was that the people asking these questions weren’t confused. A lot of the regulars on these forums are intelligent, engaged people who have built their own spreadsheet models, taught themselves UK pension tax rules, and help each other work through specific edge cases. They didn’t need the financial industry to explain retirement to them. What they needed was better tooling than a free calculator or a half-working US product, and that’s not what they had.

The financial industry consistently underestimates this group. The products that exist are either designed for people who know nothing (and so are oversimplified to the point of uselessness) or aimed at professional advisers and priced accordingly. There’s a gap in the middle for a serious tool aimed at self-directed investors who want to do the work themselves. FutureClear is an attempt to build for that gap.

What I believe

The underlying view I have is simple enough: most people in the UK advice gap are capable of modelling their own retirement, provided they have enough knowledge of what questions to ask and the tool they’re using is good enough. Advisers are still useful for the decisions where accountability matters or where a specific piece of expertise is needed. But a lot of the modelling work is something people can and should do themselves, and even when someone is going to see an adviser, walking into that meeting with your own numbers already laid out makes it a much more productive conversation.

FutureClear is built around that “education plus tools” philosophy. We provide a wealth of free (and jargon-free) content to help you understand the concepts involved in modelling your retirement. And we provide an app you can use to do it yourself. Enter your data, change some assumptions and see the effects instantly. It won’t recommend a product for you or tell you whether an outcome is good or bad. The job of the tool is to compute consequences and display them honestly. What you do with that is yours.

Where we are now

The core simulation works. The engine models SIPP, ISA, GIA, cash, property, and many other asset types; runs year-by-year projections with per-partner UK tax calculations; and has a Monte Carlo mode that runs a thousand randomised simulations to show the range of outcomes. I’m close to opening it up to a small beta group. There’s still a lot of work to do. More asset types I want to support, more event types for life transitions, a proper side-by-side scenario comparison view, and some polishing around how the results are presented. I’m building the missing pieces methodically because this is the kind of system where a calculation bug shows up as a wrong financial answer, and that’s not a kind of bug I’m willing to ship.

The beta itself will be small — probably a few dozen people drawn from r/UKPersonalFinance and r/FIREUK, plus the people who’ve already registered interest on the waitlist. I don’t know what I don’t know about how other people’s situations will map onto the current model, and the point of the beta is to find out. If something doesn’t fit or doesn’t work, I’d rather hear it now than after launch. Once that gives me enough signal that it’s doing the job for real users, and once the obvious gaps are filled, I’ll open it up more broadly.

If you spend your weekends trying to build retirement models in a spreadsheet, or if you’ve tried and given up because the UK tax side is too fiddly, FutureClear is the tool I wish I’d had when I started. If you’d like to try it, feel free to join the waiting list on our homepage. We won’t spam you with marketing - just an email or two to let you know the beta is open and to ask for your feedback.

— Darren